Uncertainty is inevitable. After all, no one can tell the future. But, sometimes, our hunches (and research) about the future are far less predictable or clear-cut. This was especially true for most businesses during the crisis caused by Covid. But you also find this happening all the time in specific industries or sectors as cultural, economic, and legislative factors change the playing field and threaten the way a business operates.

In these periods of time where there is a crisis or where the future is far less predictable than normal, an organization needs to be able to cut through some of the fog of uncertainty while also planning for an unknown future. There are four key activities that can provide both stability and direction.

Conserve: keep only what you need in order to survive.

Adapt: explore ways to sustain your organization in the current situation.

Innovate: design new products, services, and offerings for existing and new customers.

Shift: change internal cultures, brand perceptions, and a narrative to reflect the new reality.

I am going to explore each in this post with the bulk of the emphasis on Innovate since this is the hardest to work towards during times of crisis and uncertainty and where our work at FiveStone centers.

Conserve

Keep only what you need in order to survive.

In most cases of deep uncertainty, an organization needs to evaluate its current operations and look for ways it can trim. This primarily looks like a reduction in activity such as cutting spending, reducing team size, abandoning physical spaces, cutting product lines, etc.

The conservation effort not only ensures the long-term survival of the organization but also makes it easier to make necessary pivots to strategy later.

Adapt

Explore ways to sustain your organization in the current situation.

Once the necessary conservation measures are in place, organizations can start to adapt to the current reality and look for new short-term operating models. We saw this a lot during Covid as businesses adapted quickly to work from home or they spun up entirely new offerings to sustain themselves during shutdowns.

Adapting doesn’t need to mean permanence. You are looking for short-term efforts that keep the business going and appropriately respond to the external factors driving the uncertainty.

Innovate

Designing new products, services, and offerings for existing and new customers.

Innovating is always challenging; this is amplified during a crisis moment or period of uncertainty. To help, I’ve created four steps you can work through. Of course, every organization should always be innovating in some way or another. So, if you already have an innovation process, you can layer this on top. If you don’t have a process for innovation, then use these steps as a starting point.

Step One: Evaluate your situation and risk tolerance

The first thing is to evaluate how vulnerable you think your organization is to the crisis or how much you need to change to remain sustainable in an uncertain future.

If our starting assumption is that a crisis and uncertainty will force change, then the risk assessment needs to examine the risks of not changing anything, making minimal changes, and making major changes. Regardless of what your actual risk tolerance is, you will need some level of risk acceptance in order to manage through crisis and uncertainty.

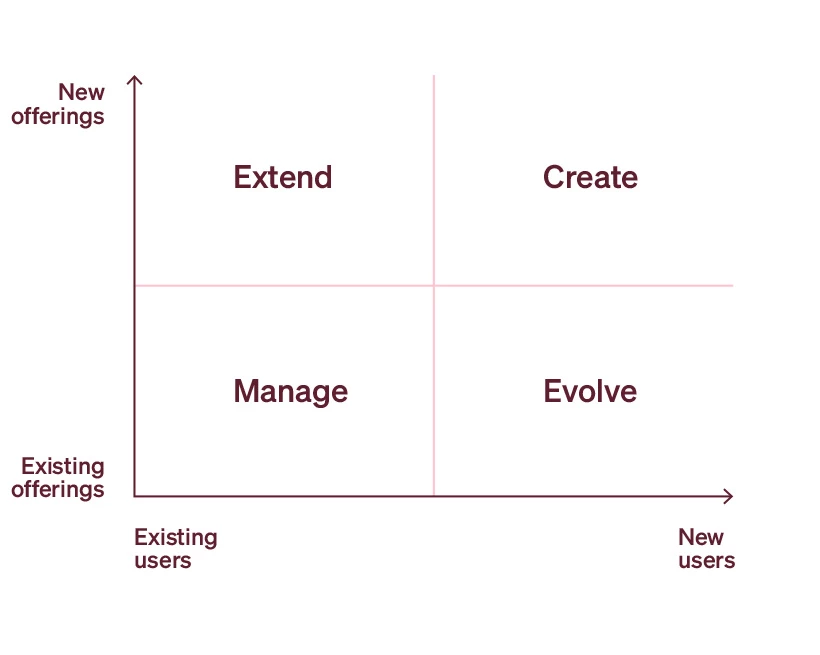

Setting your risk tolerance allows you to identify the ways in which you will explore the new future. The design agency, IDEO, talks about growth in terms of managing, evolving, extending, or creating areas of growth. This can be a good tool to help set your risk tolerance and frame the conversation for innovation.

Do you want to only make a few adjustments (manage)? Make larger changes to your existing model and strategy in order to attract new customers (evolve)? Create something new for your existing customers (extend)? Or, do you want to reimagine your entire offering (create)?

For a simple example, let’s imagine a small neighborhood restaurant currently open for dinner and dine-in seating. Rent in the neighborhood is rising, and the owner thinks their rent may rise in the next 12 months.

Manage: Update menu and pricing to include specials of the day.

Evolve: Open for lunch to draw in the business crowd.

Extend: Offer delivery services to the neighborhood.

Create: Rent a “ghost kitchen” in a new part of town and offer delivery-only options.

Likely, when you evaluated how to conserve and adapt, you focused on innovation that falls into the manage quadrant. As an example, you quickly cut underperforming products and services, scaled-up offerings that were relevant, and perhaps thought of new ways to use existing products to help your existing customers. This is great for organizations with a low-risk tolerance and short horizons for change.

However, most organizations will want to start thinking about longer-term changes. This means that your innovation work will need to fall in the evolve, extend, and create quadrants. Of course, this takes a higher tolerance for risk. But so does not thinking big enough.

Step Two: Inventory your assets

Over time, every organization has accumulated a set of assets. These are the starting blocks and tools you can use to build the future. These assets include things such as financial and social capital, infrastructure, intellectual property, business pipelines, trusted partners, existing contracts, physical space, and team.

These assets help you conserve and adapt to the current situation. But, not all assets will translate to the new future. They may end up being tools that worked only in your old playbook.

In this step, you are simply taking an inventory count. Not evaluating the value of those assets in the future; you will do that later in Step Four.

Step Three: Acknowledge your assumptions

Just like your organization has accumulated a set of assets, you have also built much of what you do from a set of stated or unstated assumptions. These assumptions drive how you think and operate.

These assumptions might sound like “people want to gather in large groups,” or “my product is in a category all by itself,” or “we will always need an office,” or “people use our service because they trust us.”

Use the following categories and list 2–3 key assumptions in each:

Assumptions about your unique value proposition(s)

Assumptions about your competitors

Assumptions about your audience's needs

Assumptions about your distribution channels

Assumptions about your operational expenses

To help, start with your asset list and ask yourself why you have that asset. What assumption drove you to, for example, move your supply chain overseas? Or, why did you sign a seven-year lease on an office space? Or, why did you build a strong sales team of consultants?

Step Four: Sketch your range of futures

In uncertainty, part of the job of innovation is to imagine a set of possible futures that could impact your organization. By imagining multiple futures (no more than 4–5 discreet options), you eliminate a binary view of decision-making while also removing the temptation to wait until you have enough information in front of you to start planning.

An example of a few futures sets that an organization might build would be:

A new set of laws change how our industry is regulated

Supply chains regularly closed for long periods of time

Changes in consumer mindsets make our existing product no longer relevant

Digital platforms change the way we conduct business

Within each future set ask:

What is prompting the imagined future to exist?

What are the biggest areas of uncertainty?

What opportunities might exist for you?

What barriers are there?

Challenge your assumptions

As you think through the future, you can challenge your existing assumptions and evaluate how well you think each might hold up in each imagined future. Something like “people use our service because they trust us and so we built a strong team of sales consultants” may very well hold up. But, if you are in the business of live events, will an assumption that people will still want to gather in large groups hold up in your sketched future?

The point isn’t to definitively say “yes” or “no” to each assumption; that’s impossible. Instead, challenge the assumption. A few challenger questions:

Was our organization built on this assumption?

How important is this assumption to our current strategy?

If we were to start our organization today, would we build off this assumption?

Once the moment of crisis is over, will we still hold this assumption?

With that said, some assumptions you are holding will need a tighter grip. These are the core assumptions that shape your vision, mission, and values. (Be careful not to confuse your mission and your strategy.) These core assumptions should stay and will help shape your view of the future and your strategy within it.

A note about innovation during crisis

As you start to answer the questions that frame your future sets, start a process by which you can evaluate new ideas and strategies that will work within each set. A typical innovation process (such as Stanford’s d.school process) will work great. Work through some form of this process for each of your 4–5 future sets.

Typical innovation methods operate within some structure of known parameters. During a crisis, however, many of those parameters are no longer well defined. This makes the process more challenging. Hold the process loosely and adjust to accommodate the reality of your situation, keeping a few things in mind.

First, when talking to potential customers during a moment of crisis, you will want to keep in mind that they are also facing uncertainty. This means that whatever you observe is clouded by their own set of fears. So, particularly during a crisis, fieldwork and analysis must be carefully designed and executed to move past the heightened feelings of uncertainty.

This may also mean that you present prototypes that work well in the current state but that you can easily imagine working in your future state. For example, prototyping something in a digital space that could also work in a physical environment. Or a pricing model that works in multiple future sets, including if nothing changes.

Next, it will be tempting to look at trend lines emerging during the crisis and ideate around those. For example, during Covid, while people were staying at home, there was a huge demand for tools that connect people virtually. But there was no way to know if that trend would stick once Covid normalized. One way to evaluate this is to determine if this trendline existed pre-crisis. If so, then maybe that trend will continue. If not, then perhaps it is just a blip so tread lightly.

Work towards the future

As you finish your innovation process, map valid ideas back to your future state and start outlining what new assets you might need and what assumptions will hold up.

If the shift to move to the new future is large enough, you may choose to start building a strategy for it now. The point is to act quickly once more of the future comes into focus or to have such a strong starting point that you can actually shift the market into your future set.

Based on what you learned during the innovation process, edit and add to the answers you outlined at the beginning of step four and while adding a few more:

What signals in the market indicate a particular future set is more likely than another?

What factors would cause your organization to respond?

Which of my current assumptions hold up and which don’t?

Which of my assets are helpful and which will I no longer need?

What new assets will you need to build?

Once you work through all four steps, for each future you should be able to organize your thoughts into a structure that looks like this:

Name of future

Hypotheses that leads to this future

Areas of uncertainty

Areas of opportunity

High-level strategic intent for operating in that future

Triggers that make this future more and/or less likely

Target customer in this future

Products, offerings, services that you can offer

Barriers to operating in this future

A global non-profit and a new future

A few years back, FiveStone worked with a global non-profit that had been executing against the same basic strategy for the last 40 years. Their strategy involved a team of speakers (asset) that conducted small and large-scale in-person events (assumption) to deliver content (asset).

We worked with them for two years, leading some light innovation work to help move them to a digital offering (evolve/extend). Any other strategic shift that did not use their current assets, or work with their current assumptions, was off the table.

Then, Covid.

At the very beginning of Covid, we met with them to discuss the weeks ahead and what this meant for their current strategy of in-person events. We discussed their risk tolerance, assets, and assumptions. In doing so, the organization was able to self-realize a few things:

Their tolerance for risk was much higher than it was just a few weeks ago. They realized that their core assumption (gathering people) was going to change.

Their primary asset (the individual speaker) was still valuable.

Until COVID-19, they had only explored a single future where their current primary asset could still work. They needed to explore multiple futures.

None of this meant that they needed to abandon their strong assets. But, in their case, it did mean that their driving assumption wasn’t going to hold true. Even though their mission stayed the same, the assumption that drove their strategy needed to change.

So, the big questions they needed to explore were: What futures can we see that need new assumptions? Will our assets work if that future plays?

Shift

Change internal cultures, brand perceptions, and a narrative to reflect the new reality.

At some point, the time will come to march forward into your new future. This will require making shifts that bring your organization and customers into your new reality.

This needed shift will vary based on what comes out of the previous steps. But typically, it looks like internal change management, developing a new set of metrics, building the right team, and updating external communications (e.g., narrative, branding, marketing, etc.).

Ask yourself how you might shift culture and brand perceptions during these moments of uncertainty. This may highlight aspects of your vision that inspire, encourage, and offer hope to your audience.

Thanks to Dave Blanchard, Steve Graves, Bonnie Zimmerman, and Sajan George for their feedback and help in shaping the article. This McKinsey article also helped provide some framework and thinking.

The FiveStone team is now part of Whiteboard.

Since 2001, we have worked with some of the most courageous organizations on the planet. We've walked alongside these organizations by offering strategy, branding, and campaigns to bring about positive change in the world.

As we think about how we might continue to live out our mission—“amplifying positive impact”—over the years ahead, we are excited to announce that we are joining forces with Whiteboard.

Whiteboard is an award-winning creative agency and Certified B-Corp. Like FiveStone, they believe in the power of Design to make the world a better place. It is clear to us that by bringing together the power of our strategic focus with their strong digital offering, we can truly build—as Whiteboard says—”the world that ought to be.”

We are thrilled to join Whiteboard and cannot wait to bring Whiteboard’s full suite of services and offerings to all our partners.

See more about Whiteboard here or visit the archived FiveStone site here.